Helen O'Kane

Deal Advisory Partner - M&A

The UK’s Health and Social Care sector continues to demonstrate its resilience and fundamental ability to deliver high quality care for the most vulnerable in society. It has faced significant challenges, including COVID and the recent cost and workforce pressures, and now looks set to deliver the growth in services required to support the strong, underpinned demand.

Investors are looking beyond shorter-term challenges and continue to be attracted to the sector, with a focus on creating platforms delivering care of the highest quality. This offers established operators the opportunity to deploy capital in developing new technologies, improve ESG processes and invest in the people, technology, and governance to deliver care of the highest quality. This provides management with a number of strategies available to pursue in order to continue to grow and develop their businesses.

When referring to health and social care, we are focusing on the core sub-sectors of Elderly residential care: market size £19.6bn, Adult specialist care: market size £14.5bn, Children’s residential, special education and foster care services: market size £9.6bn, and Home Care: market size £11.5bn.

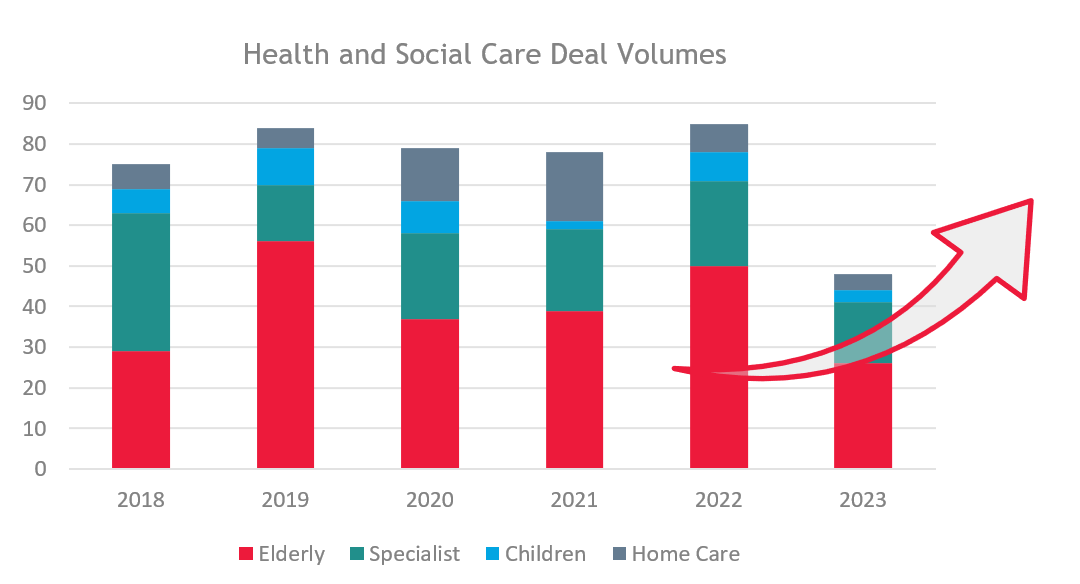

Coming out of the pandemic deal volumes continued to rise, as illustrated over 2021 – 2022, but dipped significantly in 2023. Across the sector 2023 was impacted by staffing and inflationary pressures, along with volatility in the cost of capital which led to deals taking longer, coming under more scrutiny and an element of misalignment between vendor and buyer value expectations.

The tail end of 2023 saw interest rates stabilise and inflation begin to fall, providing the M&A market with confidence heading in to 2024. Current conversations with operators and investors support this, with renewed appetite to progress investments.

Residential elderly and specialist care sectors have been, and will continue to be, supported by real estate investors, with REITs being significant investors across the elderly care sector. A key feature of these sale and leaseback transactions is the creation of asset free operating companies. As these transactions continue to be a popular route for vendors to raise funds, they also result in the growing creation of operating companies. Whilst there has been limited consolidation or acquisition of these operating companies in the UK, HC-One’s recent acquisition of Ideal Carehomes in October 2023 has highlighted the potential benefits of acquiring well managed, high quality operating companies.

Demand from financial sponsors remains strong for high quality specialist adult and children services; principally private equity and infrastructure, encouraged by the positive social impact they provide coupled with this sub-sector’s long-term care characteristics leading to relatively foreseeable revenue streams over the medium to long term.

Many of the key platforms in the specialist adult and children’s sector are backed by financial sponsors, keen to provide capital to support the further growth of high-quality operators. This will be the case for TPG and Investcorp, who acquired children’s specialist operator Outcomes First Group in December 2023 from Stirling Square Capital – highlighting the next round of investment coming into the sector.

Staffing pressures, though synonymous with the sector, appear to be alleviating more recently. Employing skilled overseas care workers was a common trend in 2023 to combat these pressures, and successfully helped operators reduce their dependency on more costly agency staff. This is likely to remain a strategy for operators in 2024, despite the element of uncertainty around on-going visa regulations.

The National Living Wage will increase by c.10% in April 2024, resulting in an immediate impact to operational costs and potentially expediting the need for operators to introduce technology efficiencies.

A key focus will also be the political landscape, with the upcoming general election expected to take place in the second half of 2024. The outcome of which will directly impact the above considerations and wider economy.

Overall, consolidation remains a strategy focus for operators looking to grow and defend against uncertainties in the sector – the buy and build model delivers benefits of scale in an inflationary environment.

Investors continue to seek, high quality, high growth, resilient investments across the core sub-sectors, as well as technology businesses that drive efficiencies across health and social care.

Alongside this, we are seeing continuing, and growing, interest from financial sponsors to invest in developing and ancillary sub-sectors, including but not limited to, non-surgical clinics, NHS insourcing & outsourcing, remote diagnostic services, specialist healthcare recruitment and remote monitoring services.

We anticipate a positive M&A outlook for 2024, as markers point to a return in transaction volumes across health and social care.

For more information, please reach out to our Health and Social Care team.

Helen O'Kane